Lecture 18: Linear Mixed Models and Generalized Linear Mixed Models

1 Learning Objectives

By the end of this lecture, students will be able to:

- Extend hierarchical normal models to hierarchical regression settings

- Derive full conditional distributions for Gibbs sampling in LME models

- Implement Metropolis-Hastings algorithms for GLMMs

- Apply hierarchical Poisson regression to real-world count data

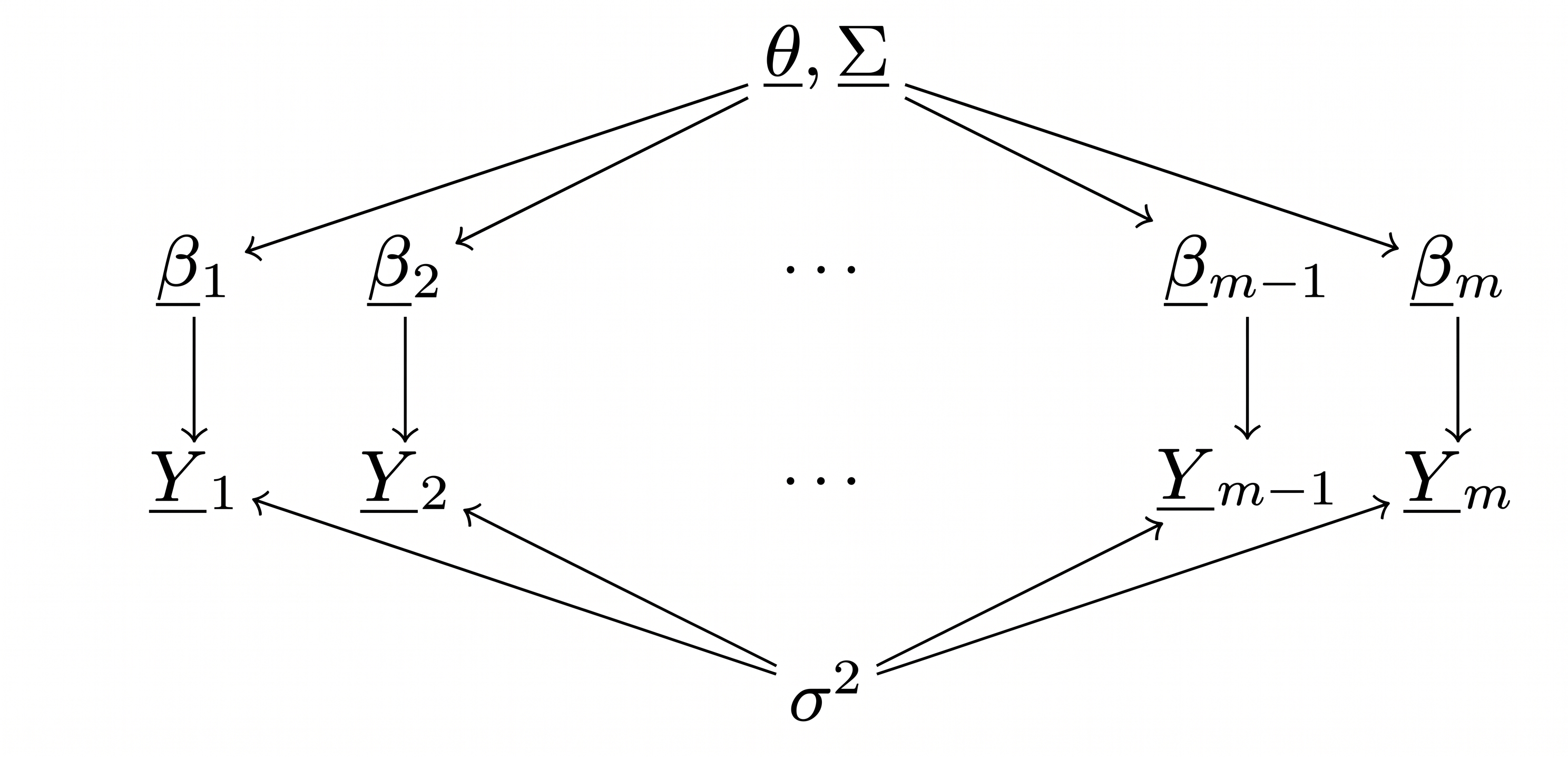

2 Linear Mixed Effects Model/Hierarchical regression

\[ Y_{i, j}=\underline{\beta}_{j}^{T} \underline{x}_{i, j}+\varepsilon_{i, j},\qquad \varepsilon_{i, j} \sim \text { i.i.d. }N\left(0, \sigma^{2}\right) \text {, } \]

Data

- \(Y_{i, j}\) = math score for student \(i\) in school \(j\)

- \(\underline{x}_{i, j}\) = covariate vector for student \(i\) in school \(j\) (intercept and SES)

- \(i \in\{1, \ldots, n_{j}\}\) index of students within school \(j\).

- \(j \in\{1, \ldots, m\}\) index of schools.

DAG for the hierarchical regression model

Where we have seen such derivations before?

\[ \begin{aligned} \underline{\beta}_{j} &\mid \underline{y}_{j}, \underline{X}_{j}, \underline{\theta}, \underline{\Sigma}, \sigma^{2} &\\ &&\\ \underline{\theta} &\mid \underline{y}_{j}, \underline{X}_{j}, \underline{\beta}_j, \underline\Sigma, \sigma^{2} &\\ &&\\ \underline{\Sigma} &\mid \underline{y}_{j}, \underline{X}_{j}, \underline{\theta}, \underline{\beta}_j, \sigma^{2} &\\ &&\\ \underline{\sigma}^2 &\mid \underline{y}_{j}, \underline{X}_{j}, \underline{\theta}, \underline\Sigma, \underline{\beta}_j &\\ \end{aligned} \]

3 Full conditional Distributions

Priors

\[ \begin{aligned} \underline{\theta} & \sim \operatorname{MVN} \left(\underline{\mu}_{0}, \Lambda_{0}\right) \\ \underline{\Sigma} & \sim \operatorname{Inverse-Wishart}\left(\eta_{0}, \underline{S}_{0}^{-1}\right) \\ \sigma^{2} & \sim \operatorname{Inverse-Gamma}\left(\nu_{0} / 2, \nu_{0} \sigma_{0}^{2} / 2\right) \end{aligned} \]

Sampling Model

\[ \underline{\beta}_{1}, \ldots, \underline{\beta}_{m} \sim \text { i.i.d. } \text{MVN}(\underline{\theta}, \Sigma) \]

Full conditional Distributions for \(\underline{\beta}_1,\ldots,\underline{\beta}_m\)

\[ \begin{aligned} \underline{\beta}_{j} \mid \underline{y}_{j}, \underline{X}_{j}, \underline{\theta}, \underline\Sigma, \sigma^{2} &\sim {MVN}(m_j,V_j)\\ V_j&=\operatorname{Var}\left[\underline{\beta}_{j} \mid \underline{y}_{j}, \underline{X}_{j}, \sigma^{2}, \underline{\theta}, \underline\Sigma\right] =\left(\Sigma^{-1}+\underline{X}_{j}^{T} \underline{X}_{j} / \sigma^{2}\right)^{-1} \\ m_j&=\mathrm{E}\left[\underline{\beta}_{j} \mid \underline{y}_{j}, \underline{X}_{j}, \sigma^{2}, \underline{\theta}, \underline\Sigma\right] =\left(\underline\Sigma^{-1}+\underline{X}_{j}^{T} \underline{X}_{j} / \sigma^{2}\right)^{-1}\left(\underline\Sigma^{-1} \underline{\theta}+\underline{X}_{j}^{T} \underline{y}_{j} / \sigma^{2}\right) \end{aligned} \]

Full conditional Distributions for \(\underline\theta,\underline\Sigma\)

\[ \begin{aligned} \underline{\theta} \mid \underline{\beta}_{1}, \ldots, \underline{\beta}_{m}, \Sigma & \sim \text { MVN}\left(\underline{\mu}_{m}, \underline\Lambda_{m}\right), \text { where } \\ \underline\Lambda_{m} & =\left(\underline\Lambda_{0}^{-1}+m \underline\Sigma^{-1}\right)^{-1} \\ \underline{\mu}_{m} & =\underline\Lambda_{m}\left(\underline\Lambda_{0}^{-1} \underline{\mu}_{0}+m \underline\Sigma^{-1} \overline{\underline{\beta}}\right) \end{aligned} \]

\[ \begin{aligned} \underline\Sigma \mid \underline{\theta}, \underline{\beta}_{1}, \ldots, \underline{\beta}_{m} & \sim \text { Inverse-Wishart}\left(\eta_{0}+m,\left[\underline{S}_{0}+\underline{S}_{\theta}\right]^{-1}\right), \text { where } \\ \underline{S}_{\theta} & =\sum_{j=1}^{m}\left(\underline{\beta}_{j}-\underline{\theta}\right)\left(\underline{\beta}_{j}-\underline{\theta}\right)^{T} . \end{aligned} \]

Full conditional Distributions for \(\sigma^2\)

\[ \begin{aligned} \sigma^{2}\mid\underline{y},\underline{X},\underline{\beta}_1,\ldots,\underline{\beta}_m & \sim \text {IG}\left(\left[\nu_{0}+\sum n_{j}\right] / 2,\left[\nu_{0} \sigma_{0}^{2}+\mathrm{SSR}\right] / 2\right), \text { where } \\ \mathrm{SSR} & =\sum_{j=1}^{m} \sum_{i=1}^{n_{j}}\left(y_{i, j}-\underline{\beta}_{j}^{T} \underline{x}_{i, j}\right)^{2} . \end{aligned} \]

Results: WWaBD

Posterior estimates of school-specific regression lines (gray) with population mean (black).

| \[\sigma^2\] | \[\theta_1\] | \[\theta_2\] | \[\Sigma_{11}\] | \[\Sigma_{21}\] | \[\Sigma_{12}\] | \[\Sigma_{22}\] |

|---|---|---|---|---|---|---|

| 849 | 1000 | 1000 | 1000 | 1000 | 1000 | 668 |

For the parameters \(\beta_{0,j}\) and \(\beta_{1,j}\) the easiest way to assess the quality of the MCMC chain is to look at the plot of the posterior mean of \(\beta_{0,j}\) and \(\beta_{1,j}\) versus their ESS for all schools.

Q: Do you see shrinkage? Which schools are shrunk more?

4 Generalized Linear Mixed Effects Model/Hierarchical GLM

In the previous section, we assumed normally distributed responses. But what if our data are counts, binary outcomes, or other non-normal types? We now extend our framework to handle these cases.

Within Sampling Model

\[ \begin{aligned} p(\underline{y}_{j} \mid \underline{X}_{j}, \underline{\beta}_{j}) & =\hspace{10cm}\\ \end{aligned} \]

5 Metropolis-Hastings=Metropolis+Gibbs

5.1 Gibbs steps for \((\underline{\theta},\underline{\Sigma})\)

\[ \\[3cm] \]

5.2 Metropolis step for \(\underline{\beta}_j\)

Sample \(\underline{\beta}_{j}^{*} \sim\) multivariate normal \(\left(\underline{\beta}_{j}^{(s)}, V_{j}^{(s)}\right)\).

Compute the acceptance ratio

\[ r=\frac{p\left(\underline{y}_{j} \mid \underline{X}_{j}, \underline{\beta}_{j}^{*}\right) p\left(\underline{\beta}_{j}^{*} \mid \underline{\theta}^{(s)}, \underline\Sigma^{(s)}\right)}{p\left(\underline{y}_{j} \mid \underline{X}_{j}, \underline{\beta}_{j}^{(s)}\right) p\left(\underline{\beta}_{j}^{(s)} \mid \underline{\theta}^{(s)}, \underline\Sigma^{(s)}\right)} \]

- Sample \(u \sim\) uniform \((0,1)\). Set \(\underline{\beta}_{j}^{(s+1)}\) to \(\underline{\beta}_{j}^{*}\) if \(u<r\) and to \(\underline{\beta}_{j}^{(s)}\) if \(u>r\).

5.3 A Metropolis-Hastings approximation algorithm

Given current values at scan \(s\) of the Markov chain, we obtain new values as follows:

Sample \(\underline{\theta}^{(s+1)}\) from its full conditional distribution.

Sample \(\underline\Sigma^{(s+1)}\) from its full conditional distribution.

For each \(j \in\{1, \ldots, m\}\),

propose a new value \(\underline{\beta}_{j}^{*}\);

set \(\underline{\beta}_{j}^{(s+1)}\) equal to \(\underline{\beta}_{j}^{*}\) or \(\underline{\beta}_{j}^{(s)}\) with the appropriate probability.

\[ \\[5cm] \]

6 Dataset: Tumor location data

Context: Spatial distribution of tumors in mice along a one-dimensional axis.

6.1 Dataset:

#### Tumor location example

load("../data/tumorLocation.RData")

Y<-tumorLocation

t(head(Y,13)) [,1] [,2] [,3] [,4] [,5] [,6] [,7] [,8] [,9] [,10] [,11] [,12] [,13]

loc1 1 0 1 1 1 0 0 1 3 0 0 0 0

loc2 0 1 0 2 1 0 0 1 0 0 0 0 0

loc3 0 0 0 0 0 0 2 0 2 1 1 0 1

loc4 0 1 0 0 2 0 0 1 2 1 0 0 0

loc5 0 0 1 0 3 0 0 0 1 0 1 2 1

loc6 0 3 1 2 2 2 0 0 0 0 1 0 2

loc7 1 1 0 0 1 3 1 1 0 0 0 1 1

loc8 1 2 0 0 2 0 0 2 0 1 0 2 2

loc9 1 4 1 2 2 0 0 0 1 2 3 4 2

loc10 3 0 2 1 5 1 2 4 4 1 3 3 3

loc11 3 3 2 4 6 2 2 4 5 3 3 3 8

loc12 3 5 3 2 6 3 6 8 7 5 4 3 4

loc13 7 3 5 8 6 7 12 7 9 11 10 8 9

loc14 8 4 5 5 7 10 5 9 9 9 9 6 13

loc15 8 7 10 4 6 12 9 11 6 7 9 7 9

loc16 11 6 10 8 9 10 5 12 9 13 13 8 11

loc17 2 4 8 9 8 9 8 9 13 5 8 13 16

loc18 3 2 9 7 8 9 6 9 6 2 4 3 2

loc19 2 2 3 2 2 4 6 3 2 1 2 1 1

loc20 1 2 0 1 3 0 1 2 2 0 0 0 0Variables: - \(Y_{j,x}\) = number of tumors at location \(x\) for mouse \(j\) - \(x \in \{0.05, 0.10, \ldots, 0.95, 1.00\}\) (20 locations) - \(j \in \{1, 2, \ldots, 21\}\) (21 mice)

Model: Hierarchical Poisson regression \[ Y_{j,x} \sim \text{Poisson}(\exp(\underline{\beta}_j^T \underline{x})) \] where \(\underline{x}\) includes polynomial basis functions of location.

\[ \\[10cm] \]

EDA: Exploratory data analysis

\[ \\[6cm] \]

Choosing predictors for the hierarchical Poisson regression

7 Results of the Tumor Location dataset analysis

#### MCMC with Caching

cache_file <- "../cache/lecture18_cache.RData"

if(!dir.exists("../cache")) dir.create("../cache", recursive = TRUE)

rmvnorm <- function(n, mu, Sigma) {

E <- matrix(rnorm(n * length(mu)), n, length(mu))

t(t(E %*% chol(Sigma)) + c(mu))

}

if(file.exists(cache_file)) {

cat("Loading cached MCMC results...\n")

load(cache_file)

cat("Loaded", nrow(THETA.post), "MCMC samples\n")

} else {

cat("Running MCMC (this may take several minutes)...\n")

#### Tumor location example

load("../data/tumorLocation.RData")

Y <- tumorLocation

## Helper functions

rwish <- function(n, nu0, S0) {

sS0 <- chol(S0)

S <- array(dim = c(dim(S0), n))

for(i in 1:n) {

Z <- matrix(rnorm(nu0 * dim(S0)[1]), nu0, dim(S0)[1]) %*% sS0

S[,,i] <- t(Z) %*% Z

}

S[,,1:n]

}

ldmvnorm <- function(X, mu, Sigma, iSigma = solve(Sigma), dSigma = det(Sigma)) {

Y <- t(t(X) - mu)

sum(diag(-0.5 * t(Y) %*% Y %*% iSigma)) -

0.5 * (prod(dim(X)) * log(2*pi) + dim(X)[1] * log(dSigma))

}

## Setup

xs <- seq(0.05, 1, by = 0.05)

X <- cbind(rep(1, ncol(Y)), poly(xs, deg = 4, raw = TRUE)); m <- nrow(Y); p <- ncol(X)

BETA <- NULL

for(j in 1:m) {

BETA <- rbind(BETA, lm(log(Y[j,] + 1/20) ~ -1 + X)$coef)

}

mu0 <- apply(BETA, 2, mean)

S0 <- cov(BETA); eta0 <- p + 2; iL0 <- iSigma <- solve(S0)

THETA.post <- SIGMA.post <- NULL

set.seed(639)

for(s in 1:50000) {

Lm <- solve(iL0 + m * iSigma)

mum <- Lm %*% (iL0 %*% mu0 + iSigma %*% apply(BETA, 2, sum))

theta <- t(rmvnorm(1, mum, Lm))

mtheta <- matrix(theta, m, p, byrow = TRUE)

iSigma <- rwish(1, eta0 + m,

solve(S0 + t(BETA - mtheta) %*% (BETA - mtheta)))

Sigma <- solve(iSigma)

dSigma <- det(Sigma)

for(j in 1:m) {

beta.p <- t(rmvnorm(1, BETA[j,], 0.5 * Sigma))

lr <- sum(dpois(Y[j,], exp(X %*% beta.p), log = TRUE) -

dpois(Y[j,], exp(X %*% BETA[j,]), log = TRUE)) +

ldmvnorm(t(beta.p), theta, Sigma, iSigma, dSigma) -

ldmvnorm(t(BETA[j,]), theta, Sigma, iSigma, dSigma)

if(log(runif(1)) < lr) BETA[j,] <- beta.p

}

if(s %% 10 == 0) {

THETA.post <- rbind(THETA.post, t(theta))

SIGMA.post <- rbind(SIGMA.post, c(Sigma))

}

if(s %% 10000 == 0) cat("Iteration", s, "\n")

}

save(THETA.post, SIGMA.post, BETA, file = cache_file)

cat("Results saved to:", cache_file, "\n")

}Loading cached MCMC results...

Loaded 5000 MCMC samples## MCMC diagnostics

load("../data/tumorLocation.RData")

Y <- tumorLocation

xs <- seq(0.05, 1, by = 0.05)

X <- cbind(rep(1, ncol(Y)), poly(xs, deg = 4, raw = TRUE))

m <- nrow(Y)

p <- ncol(X)

library(coda)

round(apply(THETA.post,2,effectiveSize),2) X X1 X2 X3 X4

674.33 1003.23 1092.27 1128.81 1145.48 #### Different posterior regions

eXB.post<-NULL

for(s in 1:dim(THETA.post)[1])

{

beta<-rmvnorm(1,THETA.post[s,],matrix(SIGMA.post[s,],p,p))

eXB.post<-rbind(eXB.post,t(exp(X%*%t(beta) )) )

}

qEB<-apply( eXB.post,2,quantile,probs=c(.025,.5,.975))

eXT.post<- exp(t(X%*%t(THETA.post )) )

qET<-apply( eXT.post,2,quantile,probs=c(.025,.5,.975))

yXT.pp<-matrix( rpois(prod(dim(eXB.post)),eXB.post),

dim(eXB.post)[1],dim(eXB.post)[2] )

qYP<-apply( yXT.pp,2,quantile,probs=c(.025,.5,.975))2.5%, 50% and 97.5% quantiles for \(\exp(\underline{\theta}^T \underline{x})\), \(\exp(\underline{\beta}^T \underline{x})\) and \(\{Y \mid \underline{x}\}\)

#### Figure 11.5

par(mar = c(2.75, 2.75, 2, 0.5), mgp = c(1.7, 0.7, 0))

par(mfrow = c(1, 3))

# Panel 1

plot(c(0,1), range(c(0, qET, qEB, qYP)), type = "n",

xlab = "location", ylab = "number of tumors",

main = expression("Population mean " * e^{theta^T * x}))

lines(xs, qET[1,], col = "black", lwd = 1)

lines(xs, qET[2,], col = "black", lwd = 2)

lines(xs, qET[3,], col = "black", lwd = 1)

# Panel 2

plot(c(0,1), range(c(0, qET, qEB, qYP)), type = "n",

xlab = "location", ylab = "",

main = expression("Group-specific " * e^{beta^T * x}))

lines(xs, qEB[1,], col = "black", lwd = 1)

lines(xs, qEB[2,], col = "black", lwd = 2)

lines(xs, qEB[3,], col = "black", lwd = 1)

# Panel 3

plot(c(0,1), range(c(0, qET, qEB, qYP)), type = "n",

xlab = "location", ylab = "",

main = "Predictive Y|x")

lines(xs, qYP[1,], col = "black", lwd = 1)

lines(xs, qYP[2,], col = "black", lwd = 2)

lines(xs, qYP[3,], col = "black", lwd = 1)

Discussion Questions:

- Why is the predictive interval (right panel) wider than the population mean interval (left)?

- What does the middle panel describe?

- At which locations is tumor count highest? Does this match the EDA?

8 Summary: LMM vs GLMM

| Aspect | LMM | GLMM |

|---|---|---|

| Response | Continuous (Normal) | Count, Binary, etc. |

| Link function | Identity | Log, Logit, etc. |

| \(\beta_j\) sampling | Gibbs (conjugate) | Metropolis-Hastings |

| Computational cost | Lower | Higher |

| Example | Math scores ~ SES | Tumor counts ~ location |

9 Key Takeaways

Hierarchical Regression: Extends hierarchical models to include covariates, allowing both intercepts AND slopes to vary by group.

Shrinkage: Group-specific estimates \(\underline{\beta}_j\) are “shrunk” toward the population mean \(\underline{\theta}\), with more shrinkage for groups with less data.

GLMMs: For non-normal responses, we replace Gibbs steps for \(\underline{\beta}_j\) with Metropolis-Hastings steps.

Mixing Issues: Hierarchical models can have poor MCMC mixing. Check effective sample sizes and consider:

- Longer chains

- Reparameterization (non-centered parameterization)

- More sophisticated samplers (HMC via Stan)